From the financial crisis to Russia’s invasion of Ukraine, Britain has borrowed and spent its way out of every jam. The bill for that is becoming a worry all its own.

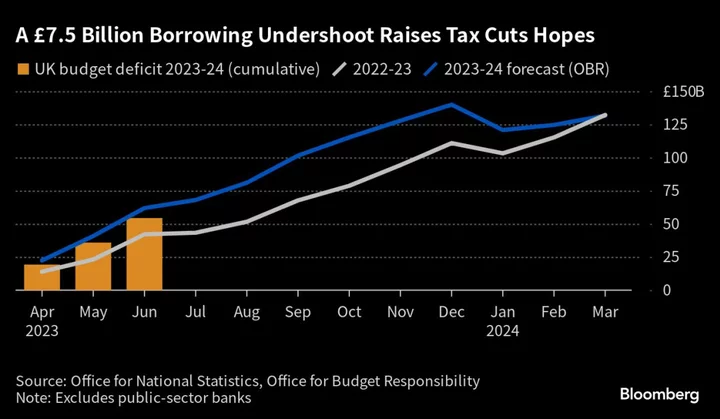

The UK’s public debt load has soared by more than 40% to almost £2.6 trillion ($3.3 trillion) since the pandemic struck, leaving the country owing more than its entire annual economic output for the first time since 1961. A heavy reliance on index-linked bonds at a time of high inflation also means Britain will pay more to service liabilities than any other advanced economy.

While big spending has helped the Conservative-led government cushion the political blow of recent setbacks, it threatens to damp investment and send the UK into a negative spiral that could last years. Last month, the Office for Budget Responsibility warned that debt could balloon to more than three times gross domestic product over the next half century without action.

The outlook has reignited questions about the UK’s credit rating, especially after Fitch surprised Wall Street and the White House by stripping the US government of its AAA status. A UK downgrade would undermine Prime Minister Rishi Sunak’s effort to rebuild Britain’s fiscal credibility after his predecessor, Liz Truss, triggered a bond-market crash a year ago by promising huge unfunded tax cuts.

The pressure is being compounded by a selloff in bonds amid aggressive rate hikes by the Bank of England to quell inflation. The yield on the 10-year benchmark this week rose above 4.70% to its highest since 2008. The UK bond market is among the developed world’s worst performers this year.

Sunak and his main rival for the prime minister’s job after an election expected next year — Labour leader Keir Starmer — have few options. Economic growth is forecast to remain flat through next year, the National Health Service is stretched to breaking point and the tax burden is already at a 70-year high.

“There is not an easy way out of the current situation,” warned Maxim Rybnikov, lead UK sovereign analyst at S&P Global Ratings. “The fiscal picture is weighing the rating down at the moment.”

The three main credit-rating firms are due to update their assessments of the UK over the next four months. Moody’s and S&P Global Ratings are scheduled to make their announcements on Oct. 20, with Fitch following on Dec. 1.

Mike Cudzil, a portfolio manager at Pacific Investment Management Co., said the US downgrade served as a reminder that “risks related to deficit spending and debt sustainability, which tend to lie dormant, can arise and spark concerns.”

Unlike the US, the UK has no unblemished status to lose. Moody’s and Fitch stripped the country of its top rating a decade ago, followed by S&P in June 2016, days after Britons voted to leave the European Union. The UK still enjoys an investment-grade rating with all three agencies.

Sunak has made reducing the country’s debt burden one of five key pledges, despite near daily calls for tax cuts and spending increases to boost the stagnant economy. Chancellor of the Exchequer Jeremy Hunt will next have a chance to address the issue in an autumn budget statement expected in November.

The most recent ratings action for the UK was positive: S&P revised its outlook to stable from negative in April. But Moody’s and Fitch, which highlighted the UK’s inflation-linked debt dilemma in a report last month, have kept the country on a negative outlook since Truss’s “mini-budget.”

While the risk of another downgrade is unclear, investors say the impact on UK assets could be more severe than it was for the dollar and US Treasuries, perennial safe havens.

“The UK is more susceptible to sudden debt-sustainability concerns because the pound, unlike the US dollar, is not the world’s dominant reserve currency,” said Sam Zief, head of foreign-exchange strategy at J.P. Morgan Private Bank. “Debt sustainability doesn’t impact markets until it does.”

Index-linked gilts were first issued in the 1980s under then-Prime Minister Margaret Thatcher, as the country struggled to clear the mark of taking an International Monetary Fund loan in 1976. While a Treasury paper from the time shows officials knew about the risks of tying debt to inflation, such bonds accumulated over decades of low inflation.

Linked gilts now account for a quarter of outstanding UK bonds. That’s double the share of Italy, the next largest issuer among advanced economies.

Britain faces a debt-interest bill of 10.4% of revenue this year, the largest share in the developed world, according to Fitch. Meanwhile, debt is forecast to jump to 105% of GDP by 2025.

“If inflation becomes entrenched, this will become more of an issue,” said Eiko Sievert, director of sovereign and public sector at Scope Ratings. “If the expectation is that next year we could have a very sharp fall in inflation pressures, then this whole debate around index linked gilts being a severe burden on public finances will become more muted.”

But it was string of shocks over the past 15 years that pushed Britain so deep into the red. Before the financial crisis began in 2008, UK debt stood around a relatively modest 35% of GDP. Then came bank bailouts, the pandemic and, most recently, Russia’s invasion of Ukraine.

The Conservative government opened its coffers, spending £376 billion to prop up businesses and households during the pandemic, according to the National Audit Office, including £70 billion on a furlough job-protection program. Another £70 billion was spent on support for energy bills and other payments as natural gas prices soared in the wake of Russia’s war.

Although inflation has slowed, the UK’s public finances will remain under pressure. Next year’s state pension bill is on track to rise as much as 8.2% under the government’s “triple lock,” which guarantees that benefits will rise at the same pace as wages or inflation, whichever is higher.

That will cost taxpayers around £10 billion, according to online investment service Interactive Investor. Surging numbers of sick working age benefit claimants will cost the state another £15 billion in lost taxes and higher welfare, the government’s independent forecaster said last month.

For now, the BOE’s efforts to bring prices under control are making things worse. Higher rates are compounding losses as the central bank reduces vast bond holdings amassed during more than a decade of quantitative easing to support the economy. Losses, which will fall on the taxpayer, are expected to hit over £150 billion over the next 10 years.

One concern is that the Conservatives, who are trailing Labour by double digits in opinion polls, might be tempted to loosen the purse strings. Some Members of Parliament are urging Sunak to cut taxes before the election.

Much is riding on what happens in the two budgets due in the fall and spring, said Bruna Skarica, UK economist at Morgan Stanley. “If the Treasury tries to do something like ease substantially in the near term, but pledge cuts in the medium-term, some of the credit rating agencies may think that’s not very plausible.”

Hunt’s previous two budgets put off a reckoning by penciling in £30 billion of spending cuts that wouldn’t take effect into after the next election. That set a potential trap for Starmer and his would-be chancellor, Rachel Reeves, who could be left with the choice of taking the blame for painful cuts or risking another investor revolt shortly after taking power.

Starmer and Reeves have said Britain needs to grow its way out of trouble. Even so, Labour has already acknowledged that it will have to delay the start of a marquee plan to remake the economy — a pledged £140 billion investment in green industries over five years.

Further out, the numbers look bleak, such as the OBR’s warning that that debt could top 300% of GDP by the 2070s.

“In some ways, it’s a rather depressing outlook,” David Miles, a senior OBR official, said in an interview. “Something will have to adjust here unless one gets a return to the kind of productivity growth of the 80s, 90s and early 2000s.”

--With assistance from Andrew Atkinson and Joel Rinneby.

Author: Tom Rees, Alice Gledhill and Philip Aldrick