Britain’s house price slump deepened after a jump in borrowing costs and the threat of worse to come held back demand from potential buyers, one of the largest mortgage lenders said.

Nationwide Building Society said its measure of prices fell 3.8% from a year ago, the most since 2009 and quicker than the 3.5% drop the previous month. Economists had expected a slightly larger decline of 4%.

The first hard data about prices for the latest month indicate the 13 interest-rate increases from the Bank of England since the end of 2021 have strained the ability of consumers to pay more for properties. The market is now in its deepest slump since the global financial crisis more than a decade ago.

“Housing affordability remains stretched for those looking to buy a home with a mortgage.,” Robert Gardner, Nationwide’s chief economist, said in a statement Tuesday. “Nevertheless, a relatively soft landing is still achievable.”

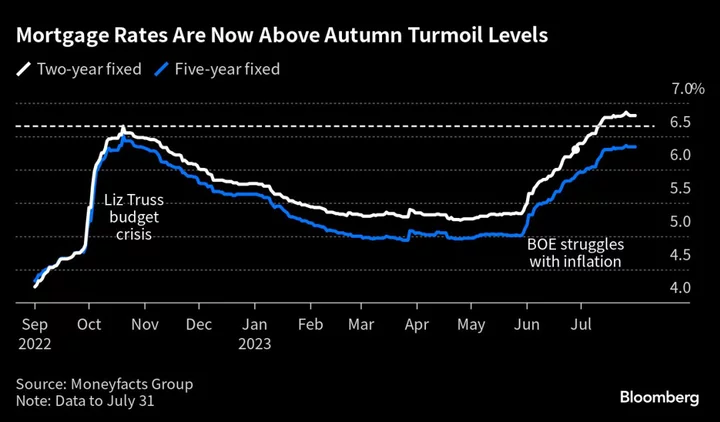

So far, prices have avoided the collapse that appeared possible last autumn, when then-Prime Minister Liz Truss’s ill-fated budget sent borrowing costs soaring to 14-year highs. In November, Nationwide had warned of a potential 30% drop in prices in a worst-case scenario.

Values based on Nationwide’s data have fallen about 4.5% since they peaked in August and now average £260,828. Prices fell 0.2% from June to July, after a 0.1% gain the previous month. The average value of a home has only fallen about 0.5% so far this year.

“We’re expecting modest falls over the rest of the year,” Andrew Harvey, a senior economist at Nationwide, said on Bloomberg Radio. “Our current forecast is for a peak-to-trough fall of around 6.5%.”

However, economists and Nationwide say that the combined pressures of higher mortgage rates and a cost-of-living squeeze will weigh heavily on property prices for the rest of this year.

Bloomberg Economics expects house prices to register a peak-to-trough decline of around 10%, implying they have a further 5.5% to lose.

Nationwide said there were 86,000 completed housing transactions in June, which is 15% below the levels prevailing a year ago and about 10% below pre-pandemic levels. Housebuilders have scaled back on projects anticipating fewer buyers.

Building supplies company Travis Perkins Plc reported lower revenues and a 31% drop in adjusted operating profit, amid “significant weakness” in the UK’s housing sector. The FTSE 250 business said Tuesday that it had suffered during the first half of the year from “a notable reduction in housing transactions” as interest rates climbed.

“There’s a lot of uncertainty among people looking to purchase a new home, so it’s no surprise prices continued to edge down on both a monthly and annual basis in July,” said Nicola Schutrups, managing director at Southampton-based mortgage broker The Mortgage Hut. “Further falls in house prices are likely for the rest of 2023.”

The BOE has hiked rates to curb inflation, which reached a four-decade high late last year. Economists are anticipating another quarter-point on Thursday to 5.25%, which would be the highest since 2008. Traders meanwhile are pricing in a 40% chance of a half-point rise this week, with rates seen approaching 6% by February.

Nationwide estimated that people earning the average wage and seeking a typical first-time buyer property with a 20% deposit would see monthly mortgage payments account for 43% of their take home pay at a 6% mortgage rate, up from 32% a year ago.

“While activity is likely to remain subdued in the near term, healthy rates of nominal income growth, together with modestly lower house prices, should help to improve housing affordability over time, especially if mortgage rates moderate once Bank Rate peaks,” Gardner said.

--With assistance from Andrew Atkinson, Julian Harris, Caroline Hepker and Stephen Carroll.

(Updates with details from the report and comment from sixth paragraph.)