UK economic growth remained weak in August, as a modest rebound from a strike-afflicted July failed to ease concerns that output would shrink in the third quarter.

Gross domestic product rose 0.2% following a revised 0.6% contraction in July, the Office for National Statistics said Thursday. Economists had expected growth of 0.2%.

The recovery partly reflects the absence of factors that depressed activity in July, mainly large-scale industrial action. Services grew 0.4%, boosted by education after teachers went on strike in July. However, manufacturing shrank 0.8% and construction contracted 0.5%, with both readings worse than economists forecast.

The figures reinforce a picture of an economy losing steam in the face of a sharp increase in borrowing costs. The Bank of England held interest rates last month, fueling speculation that the most aggressive hiking cycle since the late 1980s may have come to an end.

Doubts remain over the third quarter as a whole, with the BOE predicting growth of just 0.1% in the period. For a flat third quarter, GDP will need to rise at least 0.21% in September, the ONS said.

This looks “just out of reach,” said Sam Tombs at Pantheon Macroeconomics, given that much of August’s rise in activity was driven by a lack of strikes rather than underlying momentum in the economy. “The latest surveys point to a weather-related fall in retail sales in September and a further downturn in manufacturing output.”

A contraction during the quarter could mean the economy is already in recession. With key PMI indexes flashing warning signs and unemployment rising, Bloomberg Economics is expecting a yearlong contraction starting in the final three months of 2023.

The pound held gains after the data and was headed for a seventh day of advances, the longest winning streak since July 2020.

The latest lackluster growth figures came after BOE rate-setter Swati Dhingra warned that the UK economy has “already flatlined” ahead of further interest rate pain. She said the risk of a recession in the UK is now evenly balanced.

Recession Risks

“We think only about 20% or 25% of the impact of the interest rate hikes have been fed through to the economy,” she said in an interview with the BBC. “So I think that there’s also this worry that that might mean that we’re going to have to pay a higher cost than we should be paying.”

Activity in the housing market has also slumped, weighed down by the BOE’s string of 14 consecutive rate hikes, though a survey published today from the Royal Institution of Chartered Surveyors said new buyer inquiries and sales had bounced off recent lows as interest rates showed signs of stabilizing.

The ONS said the rise in services output was driven by the legal sector, architecture and engineering, and education, which returned to growth after two days of strikes by teachers in July. Health care also contributed to growth, with fewer doctors on strike than in the previous month. However, output in consumer-facing services slipped by 0.6%, leaving it still well below pre-Covid levels. Sports and recreation activities underpinned the weakness.

A 0.7% fall in production, which came on the back of a 1.1% slide in July, was driven by a slowdown in manufacturing.

Construction output also fell by 0.5% in August, after a 0.4% slide a month earlier. Businesses said “heavy rainfall” had led to delays in planned work - activity in private commercial and private housing decreased by 4.1% and 1.4% respectively. The fall in overall GDP the previous month was larger than the 0.5% initially estimated.

“The outlook for the economy remains lacklustre as high interest rates continue to bite,” said Yael Selfin, chief economist at KPMG UK. “Today’s data are consistent with our assessment that the economy entered a broad-based slowdown in late summer which has deteriorated further in recent months.”

Money markets show the chance of another BOE rate increase in the coming months is little more than 50-50. However, rates are expected to stay elevated for a extended period as officials keep up their battle to bring inflation back to target.

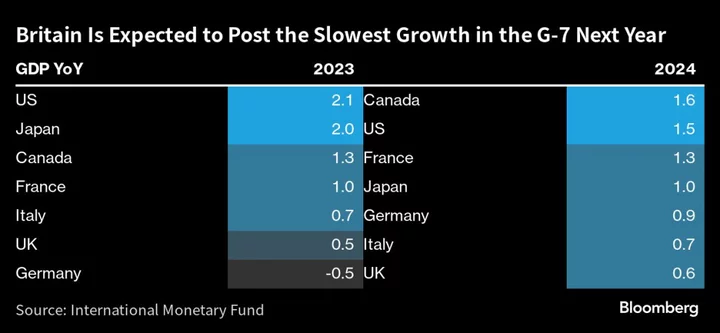

Extensive revisions announced by the ONS last month mean that the the economy is around 2% larger than previously thought, and no longer at the bottom of the G-7 growth league since before the pandemic. The laggards are now Germany and France, a development Prime Minister Rishi Sunak’s government was quick to highlight as it battles to stay in power at a general election widely expected to be held next year.

“The UK has grown faster than France and Germany since the pandemic and today’s data shows the economy is more resilient than expected,” said Chancellor of the Exchequer Jeremy Hunt. “While this is a good sign, we still need to tackle inflation so we can unlock sustainable growth.”

However, the International Monetary Fund thinks Britain will place last for growth next year, though its forecasts do not incorporate the latest revisions.

Author: Andrew Atkinson, Lucy White and Tom Rees