US stock market traders are almost completely fearless now, which has some strategists bracing for a possible selloff.

The S&P 500 Index has gained 19% this year, pushing investors off the sidelines and into the market. Traders’ stock exposure is historically high, in the top 28% of all time, according to Deutsche Bank’s analysis of rules-based and discretionary strategies going back to 2010.

Few, however, seem worried enough to hedge. Buying protection against dips in the options market is the “cheapest you likely have ever seen,” Bank of America strategists wrote in a Tuesday note. Trading volume of call options, used to wager on the market rising, outpaced puts earlier this month by the most since December 2021.

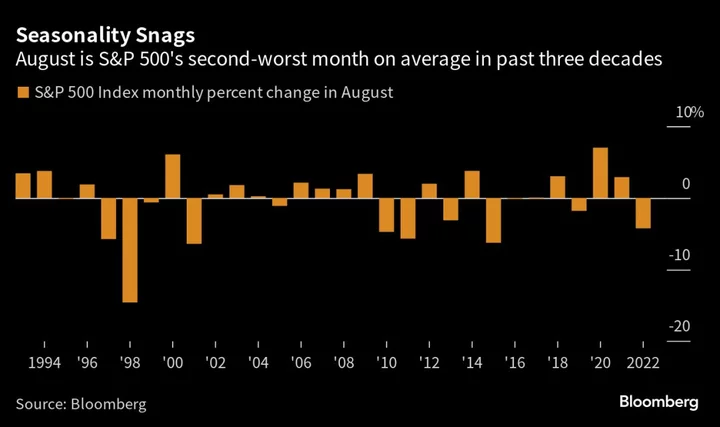

But there are reasons to be worried. The Federal Reserve is looking to engineer a soft landing after a period of inflation and intense rate hiking, an effort that’s rarely successful. On top of that, September and August tend to be the S&P 500’s worst two months of the year.

“Bullish sentiment and weak seasonality has made our contrarian antennas tingle a little bit,” said Jeffrey Hirsch, editor of the Stock Trader’s Almanac, who correctly forecast the rally after the financial crisis. “All the bears that came off the sideline are chasing this momentum and the ‘FOMO’ players are all in now, so that means it’s time to see this rally pause.”

The S&P 500’s advance has defied consensus expectations for losses to start 2023 before an eventual rebound, forcing many to rethink their forecasts. Some of Wall Street’s loudest bears, like Piper Sandler & Co.’s Michael Kantrowitz and Morgan Stanley’s Mike Wilson, have adjusted their stances.

In the options market, traders reacted to the rally in equities by showing a bias toward calls, partly fueled by an AI boom that supercharged a tech-stock advance. Across US exchanges, the volume of calls outpaced puts by more than 8 million contracts on a 10-day moving basis, the most since December 2021, Bloomberg data show.

Of course, there are reasons for the S&P 500’s rally, now on pace for its fifth consecutive monthly gain. Inflation has been slowly subsiding while the economy has stayed relatively resilient in the face of the most aggressive tightening cycle in decades.

Wall Street traders eventually got the memo, ditching downside protection and pushing the cost of hedging against drops to fresh lows. For every $100 in notional — the value an options contract covers — investors now pay only $3.50 for an S&P 500 put option expiring a year from now with a strike price 5% below current levels, data compiled by Bank of America show. That’s the least in the bank’s data going back to 2008. (Between the premium and the strike price, the contract will be profitable if the S&P 500 falls at least 8.5% a year from now.)

Whether that will happen is yet to be seen, but momentum seems to be getting stretched. The Cboe put-to-call ratio that tracks the volume of options tied to individual stocks is at the lowest level in more than a year. This historically has translated into a flat performance for the stock market over the next three months, data compiled by Goldman Sachs Group Inc. show.

Then, seasonal patterns can create an additional headwind. Over the past 30 years, September and August have been the two worst months for the S&P 500, with a 0.4% drop in the former and a 0.2% decline in the latter.

Like many on Wall Street, Luca Paolini, chief strategist at Pictet Asset Management, closed a short position on US equities earlier this month amid a relentless rally. Now neutral on US stocks, Paolini still thinks investors are underpricing potential risks to the economy.

“The market is giving us a clear signal that bullish momentum has been building,” he said. “There’s an incredible level of confidence that the Fed can manage a ‘soft landing,’ with weaker growth and lower inflation without a recession. But if something goes wrong, it will be related to that.”

Preliminary data on Thursday showed gross domestic product unexpectedly picked up steam in the second quarter, boosting confidence about the state of the economy and simultaneously fueling bets that the Fed’s campaign against inflation could go on for longer than expected. The US central bank is taking a data-dependent approach to future interest-rate hikes, Chair Jerome Powell said on Wednesday.

One potential concern is that the easy year-over-year inflation data comparisons will start to drop out later this year, says 22V Research’s Dennis Debusschere. Inflation swaps are pricing in a 3.2% advance in headline inflation in July from a year ago and a 3.6% gain in August.

Higher inflation could translate into rates not falling anytime soon.

“There is a ‘CPI-mission accomplished’ state of mind among many investors at this point, and it’s not the case,” said Nitin Saksena, head of US equity derivatives research at Bank of America. “There is this risk that the Fed will keep interest rates higher for longer, and it will cause something to ultimately break.”

--With assistance from Carly Wanna.