Yields on 30-year Treasuries are on track for their largest quarterly jump since 2009, stoking anxiety that the bond rout of the past few months could reverberate across financial markets.

The long-bond yield has risen around 85 basis points since the end of June and touched about 4.81% Thursday, the highest since 2010. Pershing Square Capital’s Bill Ackman said he would not be shocked to see 30-year Treasury yields well into the 5% barrier, during an interview with CNBC on Thursday.

An array of forces have accelerated the Treasuries slump, and investors in longer-maturity bonds, which bear the biggest interest-rate risk, have suffered the most.

A key trigger has been the Federal Reserve’s message that it will keep rates higher for longer. But the government’s increased borrowing to fund budget deficits, the move by Fitch Ratings to strip the US of its top credit grade and rising oil prices are also at work. The Bank of Japan’s willingness to let Japanese yields climb has been a factor too.

“We could see something break when you see this kind of volatility,” Thierry Wizman, director of global currencies and an interest-rate strategist at Macquarie Futures, said on Bloomberg Television on Thursday.

Ackman said energy prices and interest rates moving up remain a concern.

Losses Mount

US government debt has declined about 3.1% this quarter, for a 1.6% drop this year, according to Bloomberg index data through Thursday. Treasuries are heading for a record third straight annual loss, after sinking 12.5% last year. Long bonds have lost 12% since June.

So far, the economy and financial markets have proven relatively resilient in the face of the bond market’s struggles. While the S&P 500 Index has declined 6% from its 2023 high set in July, it’s still up 12% this year.

And yet, higher yields are tightening financial conditions at a time when headwinds are building, like the autoworker strike, the imminent resumption of student-loan payments and a potential government shutdown starting this weekend.

“One characteristic of this bear market in bonds is that there hasn’t yet been a major, negative feedback as a result of those higher yields,” said Jack McIntyre, a portfolio manager at Brandywine Global Investment Management. “We thought it was the banking issue last spring,” when several regional banks collapsed under the weight of losses on fixed-income holdings and a deposit flight.

Investors are now wondering what’s the next shoe to drop in markets, leaving them in “the fear stage” in terms of their approach to fixed income, he said.

The Fed has yet to push back against rising yields. Officials may even welcome the move because it helps cool inflation by slowing economic growth. The central bank left rates unchanged at a 22-year high last week, and officials penciled in one more hike this year.

‘Hot Mess’

Charlie McElligott, a cross-asset macro strategist at Nomura Securities International Inc., sees a scenario where the selloff could intensify, should investors such as insurance companies have to reduce their long-bond holdings to cut losses or hedge interest-rate risk.

“That universe is sitting on a hot mess of substantial unrealized losses in their portfolios, particularly from any-and-all US Treasuries purchases made over the course of the past year,” he wrote in a note Thursday.

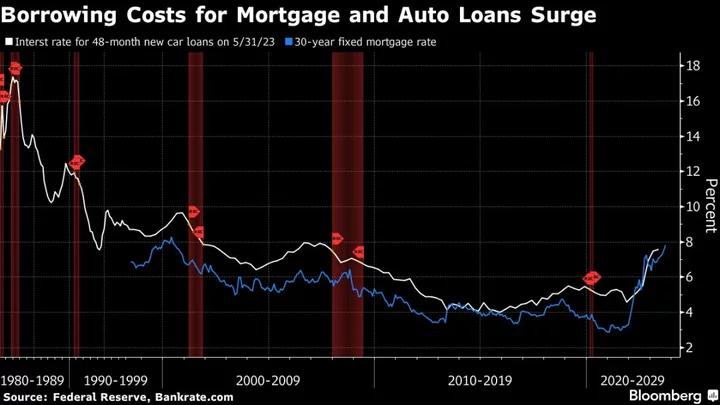

Marko Kolanovic has an alarming historical comparison in mind: the global financial crisis. The chief market strategist at JPMorgan Chase & Co. pointed out that the increase of consumer loan rates over the past two years, in percentage terms, is about five times larger than the 2002-2008 period.

“The core risk for markets and the economy is tied to the interest-rate shock of the past 18 months,” he wrote in a note this week. “History doesn’t repeat, but it rhymes with 2008.”

It all amounts to a toxic mix that has market watchers increasingly wary, with Bridgewater Associates LP founder Ray Dalio telling CNBC the US is heading for “a debt crisis.”

Some investors are stepping up their efforts to protect against a further backup in yields. The cost of using options to insure against a continued increase in Treasury rates — most notably in longer maturities — has jumped to the highest in about a year.

--With assistance from Tom Keene, Lisa Abramowicz and Garfield Reynolds.

(Updates with Ackman comments, refreshes yields, returns.)