The bond rally that erupted after this week’s US inflation report was the moment Wall Street veteran Bob Michele has been waiting for.

The J.P. Morgan Asset Management chief investment officer for fixed income has been gearing up for a bond rally since late last year, buying high-quality government bonds, credit and emerging-market debt as they fell to multi-year lows. He has long believed the US economy will enter a recession as the Federal Reserve went too far in raising interest rates.

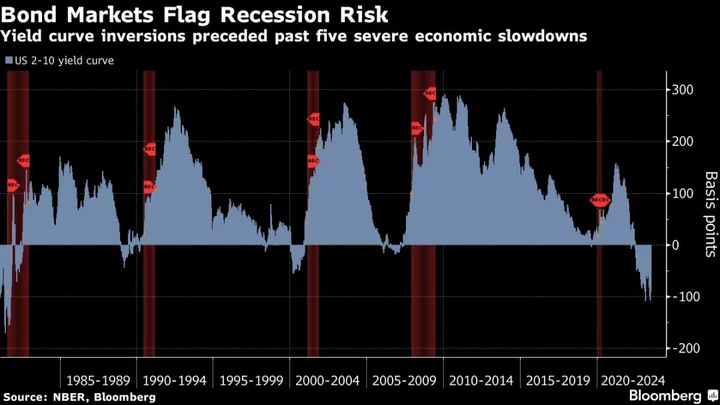

So when he saw inflation in the world’s biggest economy cooled more than economists had forecast, he was convinced this was the start of a prolonged rally. Michele, who has been in the market for more than four decades, says the deeply inverted US yield curve spells trouble and the Fed will be forced to cut rates by the end of this year.

“More and more indicators are at levels you only see in recession. We are buying every backup in yields,” said Michele. “The considerable central bank tightening is starting to bite hard in the real economy.”

His long duration position is now the biggest since the start of the pandemic.

Michele’s bullish view was repeatedly tested by markets in the past months, as stronger US economic data led investors to bet the Federal Reserve would continue to raise rates through the end of the year and keep them higher for longer. That sent Treasury yields to the highest levels since the global financial crisis, bruising investors like himself.

Michele’s JPMorgan Global Bond Opportunities Fund gained 2% this year, lagging almost 70% of its peers, according to data compiled by Bloomberg. But his longer-term track record is encouraging, with the fund outperforming 95% of its peers over the past three years and 97% in five years.

In 2019, Michele rode the bull run in US bonds, predicting that yields were “headed to zero” when the 10-year benchmark was trading at 2%. He reaped the rewards as the yield fell to 0.5% within a year.

In October 2021, when most economists polled by Bloomberg expected the Fed to hold rates near zero through the end of 2022, Michele said the central bank was way behind the curve and would need to aggressively fight inflation.

Now, Michele says it’s hard to be upbeat about the economy. A recent Fed report showed 37% of US companies are in distress, more than during most tightening episodes since the 1970s.

Other data high on his radar include gross domestic income and the Fed Senior Loan Officer Opinion Survey — both of which paint a grim outlook.

“Based on all the stress we’re seeing in the system, we’re pretty confident we’re going to see that sharp rise in unemployment,” said Michele. “It’s going to feel like a soft landing until you actually hit recession.”