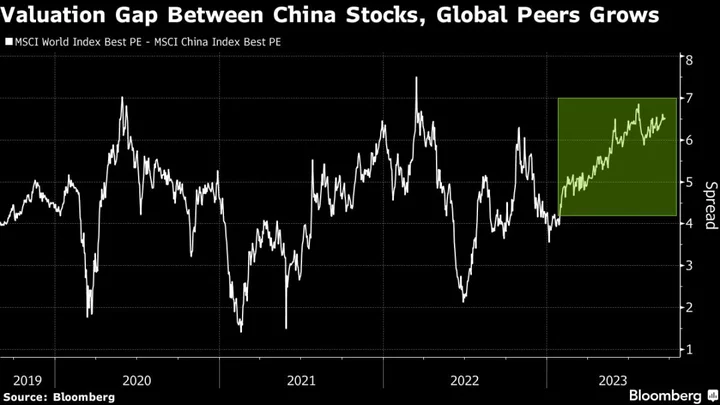

As frustration over China’s equity performance increases, some of Asia’s other major markets are emerging as more attractive alternatives for global investors.

The divergence has been on full display this week. A key Chinese stock gauge saw losses from its recent peak reach 20% just as South Korea’s Kospi flirted with a bull market and benchmarks in India approached all-time highs. Japanese stocks hit a three-decade high earlier in May while Taiwan continues to outperform most stock markets around the world.

Odds of a structural shift in Asia-focused portfolios are gaining traction as China decouples. The surge in these markets has come amid concern that China’s economic slump will drag on equities across the region. Glowing prospects for world-leading chipmakers in Korea and Taiwan, a revival of inflation in Japan and India’s booming consumption are among the tailwinds boosting their stocks just as China indexes become global laggards.

READ: Everywhere You Look in China Are Signs of More Market Misery

“There are absolutely numerous opportunities within Asia outside of China,” said Christina Woon, investment director of Asian equities at abrdn plc. “Korea gives you exposure to a great number of companies within the battery and tech supply chain, Taiwan is home to more than just TSMC, and Japan gives you access to global leaders in their fields.”

Overseas inflows into Japan have continued for seven straight weeks through mid-May, while Korea and Taiwan have netted at least $9.1 billion each this year. By contrast, global fund allocations for China have dropped back to October levels, according to HSBC Holdings Plc, and local fund sales in May slumped to their lowest since 2015.

Bullish Wall Street calls on China — dominant until a few months ago — are falling flat as a faltering economy and geopolitical tensions turn key gauges into global laggards. Manufacturing activity continued to slump in May, adding to the bleak outlook.

Fundamental Shift

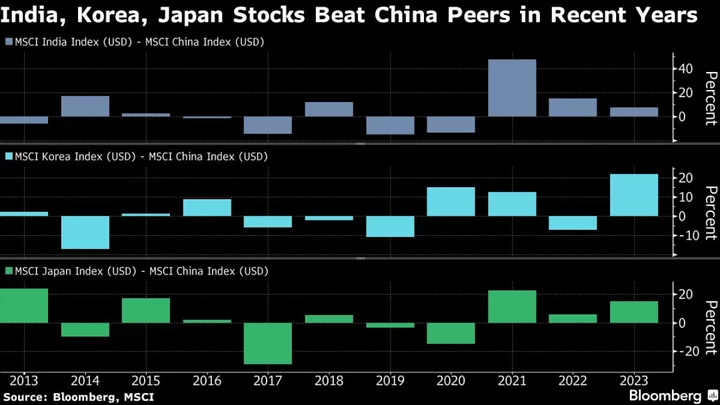

The outperformance of these other markets may be more structural as China’s population shrinks and industries mature, with Beijing’s regulatory uncertainties making any big bet a risky one. Stocks in Japan, India and Korea have beaten China peers more often than not since 2020.

“A re-allocation away from China may in fact have catalyzed a wider rally across largely dispersed parts of Asia,” said Aninda Mitra, head of Asia macro and investment strategy at BNY Mellon Investment Management. The macro picture in emerging Asia is helping, with peaking interest rates, more pressure on the US dollar and resilient Western demand, he added.

Corporate reforms underway in Japan and an endorsement by Warren Buffett have stirred great excitement toward the nation’s long-undervalued stocks. The Topix and Nikkei indexes boast double-digit gains this year, handsomely beating an Asia benchmark.

The tech-heavy markets of South Korea and Taiwan are rallying as global demand surges for all things AI and as the chip cycle is seen turning a corner. Benchmarks there too have gained at least 15% each this year. In India, a growing retail investor base and solid earnings are adding to the appeal of equities with foreign funds also piling in, helping drive the Nifty 50 Index to less than 2% away from an all-time high.

“Korea is our current favorite due to its about 60% semiconductor, component and tech exposure,” said Hartmut Issel, Asia Pacific head of equity and credit at UBS Wealth Management. “Prices have already touched cash costs, the inventory digestion process is under way” and the sector is cutting capex plans, he added.

The Asia ex-China theme has been evident in recent strategist actions. BNY Mellon Investment Management turned neutral on China last week, preferring markets that benefit from Chinese consumption such as Korea, Thailand or Singapore. Citigroup Inc.’s global allocation team on Friday changed its China call to neutral from overweight citing a lack of stimulus measures, while upgrading the rest of emerging Asia citing tech stocks’ outperformance.

To be sure, pockets of the Chinese market have seen sharp rallies such as state-owned enterprises as well as semiconductor and artificial intelligence names. And as the November-January reopening euphoria shows, losing out on any China market rebound can be painful.

As money chases markets that have momentum, valuations have become less of a concern. Korea’s Kospi and Japan’s Nikkei 225 are trading at a 23% and 17% premium, respectively, to their average price-to-forward earnings multiple over the past 10 years. Indian gauges, a perennial bugbear for being richly valued, are trading at close to 20 times.

For now though, the Chinese market’s perennial volatility and unpredictable regulatory environment means investors are being more picky.

“You need to be much more specific and targeted in terms of how you are investing within” China, Timothy Moe, chief Asia-Pacific equity strategist at Goldman Sachs Group Inc., told Bloomberg TV. “There’s a great deal of scepticism about the longer term outlook for China, then that suggests investor appetite for China in the near term is still going to be subdued.”

--With assistance from John Cheng and Charlotte Yang.