The $1.3 trillion market for reselling leveraged loans is facing its lowest profitability in years, potentially making it harder for lower-rated companies to refinance debt.

The collateralized loan obligation market — the biggest buyer of leveraged loans — is getting squeezed as funding costs rise relative to the returns on investments. That’s making it less attractive for money managers to issue new CLOs.

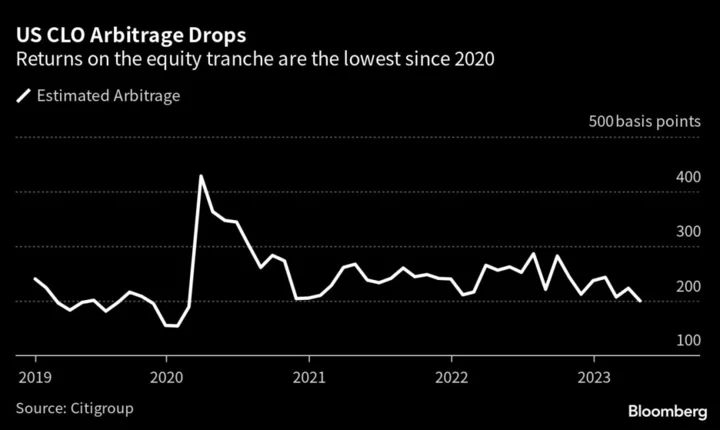

It all comes down to the arbitrage opportunity from the gap between the yields that CLO managers can earn on the loans they buy, and what they pay to finance themselves with the riskiest securities they issue known as equity. For US CLOs, that spread narrowed to just 200 basis points at the end of April, the lowest since 2020, according to Citigroup research.

It’s a big change from this time last year, when the spread was closer to 260 basis points, according to Citigroup’s data. In Europe, the arbitrage opportunity has also slumped, dropping 77 basis points in a month to 250 basis points by one measure, according to Bloomberg Intelligence.

“New issue CLO equity arbitrage looks thin,” said Tyler Wallace, a portfolio manager at Fair Oaks Capital Ltd., who buys leveraged loans to bundle into CLOs. “The current arbitrage is about half of the historical range.”

With potential profits so low, money managers aren’t creating as many new CLOs. The volume of issuance in the US has dropped around 12% so far this year from the same period in 2022, according to data compiled by Bloomberg News. In Europe, CLO issuance has fallen by a third from 2022.

It’s creating a vicious cycle because leveraged loans and CLOs rely so closely on each other. In Europe, the lack of loan supply is also pushing up loan prices in the secondary market.

European CLO arbitrage dropped in April “as tranche costs rose and new loan spreads rallied,” said Mahesh Bhimalingam, chief European credit strategist for Bloomberg Intelligence. “This will hurt near-term supply for both loans and CLOs.”

Read more: Europe’s CLO Market Is Getting Squeezed as M&A Slows Down

Within the CLO structure, it’s especially hard for issuers now to sell the equity portion — the first part to absorb any losses. But there’s also relatively tepid demand for AAA securities, an additional factor hurting the CLO arbitrage. Capra Ibex Advisors LLC, which buys CLO equity, isn’t looking at new issue CLO equity systematically anymore. Eagle Point Credit Management, which mainly invests in equity, has also avoided newly-issued debt for about nine months.

“There are better opportunities in the secondary market and in other products,” said Dan Ko, senior principal and portfolio manager at Eagle Point. “AAAs need to tighten and loan prices to drop to make the CLO equity arbitrage work. Until then, demand for leveraged loans will remain very weak.”

There are workarounds. For example, buying loans at relatively cheap prices can result in higher yields on the investment side, said Dave Preston, head of structured credit research at AGL Credit Management LP.

“There are still ways to make the CLO work,” Preston said.

And there are a handful of managers that can afford to keep selling CLOs despite the relatively small arbitrage opportunity. They are doing it through captive equity vehicles — pools of capital deployed for the manager’s own benefit — according to Citigroup strategist Maggie Wang.

Eagle Point estimates that around 85% of CLOs priced during the first quarter were done with captive equity, more than double the amount it used to be.

“If this continues, CLO managers without a captive equity investor won’t be able to get deals done and the CLO manager market will continue to consolidate,” said Michael Kurinets, chief investment officer at Capra Ibex Advisors LLC.

(Updates with comment in paragraph 9, quote in last paragraph)