It was meant to be the year China’s economy, unshackled from the world’s strictest Covid-19 controls, roared back to help power global growth.

Instead, halfway through 2023, it’s facing a confluence of problems: Sluggish consumer spending, a crisis-ridden property market, flagging exports, record youth unemployment and towering local government debt. The impact of these strains is starting to reverberate around the globe, impacting everything from commodity prices to equity markets. The risk of Fed hikes tipping the US into recession has also heightened the prospect of a simultaneous slump in the world's two economic powerhouses.

What's worse, President Xi Jinping’s government doesn’t have great options to fix things. Beijing’s typical playbook of using large-scale stimulus to boost demand has led to massive oversupply in property and industry, and surging debt levels among local governments. That’s sparked a discussion about whether China is headed for a Japan-style malaise after 30 years of unprecedented economic growth.

Exacerbating this is Xi’s more assertive approach to dealing with the US, which has added fuel to American efforts to cut China off from supplies of advanced semiconductors and other technologies set to drive economic growth in the future.

Altogether, the dynamics threaten not only to lead to disappointing growth this year, but also to thwart the Chinese economy’s momentum to surpass that of the US.

“A few years ago, it was difficult to imagine China not rapidly overtaking the US as the world's biggest economy,” said Tom Orlik, chief economist for Bloomberg Economics. “Now, that geopolitical moment will almost certainly be delayed, and it's possible to imagine scenarios where it doesn't happen at all.”

In a downside scenario — with a sharper property slump, slow pace of reforms and more dramatic US-China decoupling — Bloomberg Economics sees China’s growth decelerating to 3% by 2030.

Base Effect

China’s $18 trillion economy is struggling across a range of sectors. Data released Friday showed the economy lost more steam in June, as manufacturing activity contracted again and other sectors failed to build momentum.

In the debt-strapped southwestern province of Guizhou, officials are seeking bailouts from Beijing. In the manufacturing hub of Yiwu in coastal Zhejiang province, small businesses say sales are down substantially from 2021 levels. Over in the city of Hangzhou, the home of e-commerce giant Alibaba Group Holding Ltd., a government regulatory crackdown on the tech sector and tens of thousands of layoffs are now affecting the property market.

China’s official growth target of around 5%, which was deemed unambitious when it was announced in March, now looks more realistic. Goldman Sachs Group Inc. in June cut its forecast for China’s growth this year to 5.4% from 6%.

At first sight, in a world economy expected to grow a meager 2.8%, that doesn't look too shabby. The reality, though, is that with China still under Covid rules in 2022, a low base for comparison is flattering the headline. Netting out the base effect, growth for 2023 will look closer to 3% — less than half the pre-pandemic average, Bloomberg Economics said.

If the government continues to sit on its hands, things could get worse. In a scenario where property construction crumbles, reduced land sales hit government spending, a US recession weakens global demand and China's markets shift to risk-off mode, Bloomberg's SHOK model shows another 1.2 percentage points shaved off growth.

“We’re caught in a kind of vicious circle in the sense that you need a massive stimulus to create a little moderate impact," said Keyu Jin, an economics professor at the London School of Economics and Political Science who wrote The New China Playbook: Beyond Socialism and Capitalism.

“We have to be prepared for slower growth in the future because China is really in transition right now from industrialization to innovation-based growth," she said. "Innovation-based growth is just not that fast.”

To be sure, China's policymakers have defied the doomsayers before and could do so again. A bigger-than-expected stimulus, proactive moves to resolve bad debts, a commitment to support entrepreneurs and extending an olive branch to the US could dispel some of the pessimism.

But for now, the lack of substantial stimulus or real reform is frustrating investors. The 12% rally enjoyed by the MSCI China Index in January proved a false dawn as the gauge steadily gave back all the year’s gains. It’s now down about 6% in 2023 and Wall Street’s biggest banks are cutting forecasts to levels that suggest it will struggle to reclaim the levels seen earlier this year.

The yuan’s CFETS basket has fallen every week since late April, a losing streak unmatched since the China Foreign Exchange Trade System started compiling the data in 2015 — and enough to see the People’s Bank of China step in to prop up the currency.

Confidence Trap

At the start of 2023, optimism was high that China would see a rapid recovery in consumer spending, fueled by revenge shopping, eating out and travel. But anxiety about what weaker growth means for unemployment and incomes, combined with the negative wealth effect from a slumping property sector, has prompted people to save rather than spend.

Xiao Jin was one of the people hoping the abrupt end in December of three years of Covid Zero would mean shoppers would flock back to her toy shop in Zunyi, a city in Guizhou.

“We barely made any money in the last three years,” Xiao, a mother of two children, said outside her shop in mid-June. But “business is even worse than last year.”

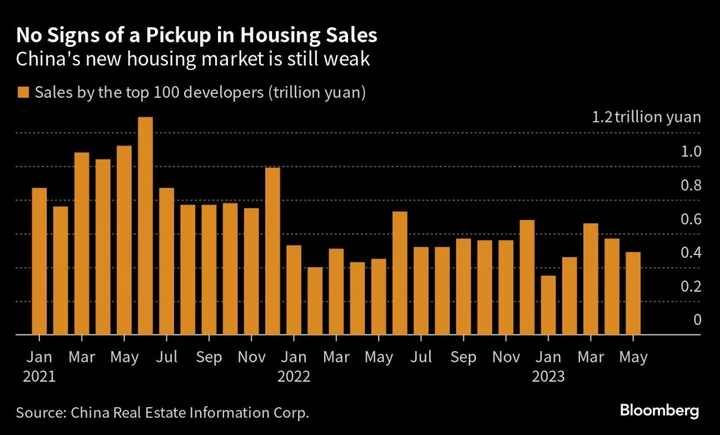

At the heart of wilting consumer sentiment is the property market. The slump followed the government's attempt to crack down on heavily indebted real estate developers in 2020 to reduce risk. That pushed housing prices down and a number of the weaker companies defaulted. Many developers stopped building houses they had already sold but hadn’t yet delivered, prompting some home owners to stop paying their mortgages.

This turbulence was a wake up call for many Chinese, who have long considered property a sure-bet investment and used it as a store of wealth.

And there’s no indication the fall in property prices is attracting the new buyers needed to kickstart a rebound. Banks advanced the smallest amount of longer-term loans to households last year in almost a decade and borrowing was down another 13% in the first five months of this year, indicating fewer people are taking out new mortgages.

Another worrying sign is youth unemployment. At 20.8%, the jobless rate for those aged 16 to 24 is the highest since China began publishing the data in 2018 and is four times the national urban rate. A big reason is the slump in services industries as a result of strict Covid rules and the decline in the property market. The tech crackdown also took away a lucrative career path for many young, ambitious graduates.

At a recent job fair in Beijing, Wu Yuanhao, 27, said he’s looking for a position in the e-commerce industry, but firms are cutting staff and pay is about 20% lower than three years ago, when he last looked for a job.

“The job searching prospects are not as good as before,” he said. “The competition is in fact very fierce.”

Exports Weaken

It’s not only domestic demand that’s disappointed. Foreign trade had been a consistent support during the pandemic as Chinese factories rushed to fill US and European orders, but it’s dwindled in recent months. Since peaking at a record $340 billion in December 2021, exports in May were down almost $60 billion and are set to continue dropping as rising interest rates weigh on growth in the US and Europe.

In Yiwu, Huang Meijuan has been selling artificial Christmas trees all over the world for more than 20 years. This year she expects sales to drop 30% from 2022’s record.

“In the past two years, customers actually placed big-value orders online as the international market was strong,” said Huang. “Now the customers are back, but they are checking around to compare prices and coming back to bargain hard.”

Fading growth momentum is contributing to China’s consumer inflation staying at close to zero. Factory gate prices have already tipped into deflation — leaving businesses with less income to repay their debts.

That economic weakness has forced Beijing to shift gears. The central bank cut interest rates in June and the State Council, China’s cabinet, said it’s discussing new support measures for the economy. Possible options include a further easing in property restrictions, tax breaks for consumers, more infrastructure investment and incentives for manufacturers, especially in the high-tech sector.

Still, property and infrastructure stimulus will probably be “targeted and moderate” given the shrinking population, elevated debt levels and Xi’s call for curbing property speculation, Goldman Sachs analysts in China wrote in mid-June.

Hidden Debts

The reason that large infrastructure-led stimulus isn’t viable anymore is clear if you walk around Zunyi or travel out of the city into the countryside. While the impoverished and mountainous province of Guizhou did need some investment, it's now awash in expensive bridges, tunnels, roads and airports. And it’s struggling to pay back the debt it took on to finance all that construction, forcing it to make pleas to Beijing about its severe debt crunch.

Zunyi, a city of 6.6 million people, is served by two different airports about an hour from the downtown. Three hours away by car, there’s another airport in the city of Liupanshui. It opened in 2014 at a cost of 1.5 billion yuan ($208 million), but the airport now has few commercial flights. On a recent visit, on a day when there were no scheduled flights, the only people in the terminal were a security guard, a few cleaners and some attendants in deserted shops who were eating lunch.

Much of the funding for these projects, and others around the country, came from local government financing vehicles — companies created by municipalities to borrow on behalf of cities, towns and provinces — with that debt not appearing on their balance sheets.

It’s this “hidden debt” that’s become a major risk for China’s local governments and a big worry for investors who have bought bonds sold by the local government financing vehicles. The International Monetary Fund estimated in February that nationwide there was 66 trillion yuan of this debt at the end of 2022, up from 40 trillion yuan in 2019, with that quick increase underscoring how local governments ramped up off-book borrowing and spending during the pandemic.

Local governments are themselves under financing pressure. They had come to rely on land sales to property developers to top up their coffers, but that source of revenue is drying up due to the housing downturn.

With the central bank now starting to cut rates, and cities across the country lowering the down-payment requirements and removing restrictions on buying multiple properties, the lackluster state of the property market might gradually change. But massive oversupply means it will take a while for any property stimulus to flow through to actual housing construction, if it does at all.

Back in Hangzhou, home prices in some neighborhoods are down almost 30% from a peak in late 2021, according to multiple real estate agents. The slump is an abrupt change for the affluent city that served as host to the Group of 20 summit back in 2016. At the time, Xi said it showcased “what has been achieved in the great course of reform and opening-up China has embarked upon.”

“I’ve never seen such a fast decline in such a short period of time in Hangzhou,” said an agent surnamed Gao who has worked in the industry in the city for almost a decade, asking to be identified by her last name because she wasn’t authorized to speak publicly. “It’s completely a buyer’s market now.”

Wang, the wife of an Alibaba employee, listed one of the couple’s two apartments in the city for sale in early June after a round of job cuts at the tech giant.

“For the first time, the layoff news made me rethink whether the mortgages we’ve undertaken are too high,” said Wang, who asked to be identified by her surname only because she was talking about a private matter. “It might be time to prepare for darker times ahead.”

--With assistance from Yujing Liu.

(Updates with manufacturing data in eighth paragraph.)