Chinese stocks are expected to see modest gains in the second half as investors grapple with just how far policy stimulus will go in turning around a faltering economy.

The benchmark CSI 300 Index of mainland shares will likely climb about 3% this quarter while Hong Kong’s Hang Seng Index may advance less than 6%, according to the median estimate of 18 analysts and money managers surveyed by Bloomberg News this week. Weak economic data were cited as the chief concern, eclipsing geopolitical risks and a potential US recession.

While the majority said the market has bottomed out, year-end projections suggest major gauges will fail to claim their peaks seen during the reopening rally. The somber outlook shows investors expect no game-changer for the sluggish stock market, with authorities remaining mum on large-scale stimulus even as they pledge support for the economy.

China is on the “brink of a self-fueling confidence trap as the initial reopening impulse starts to fade,” Citigroup Inc. analysts wrote this week as the brokerage trimmed its target on the Hang Seng Index, which comprises primarily of mainland companies. Stocks are expected to trade range-bound in the second half, with the outlook highly dependent on a basket of stimulus measures, they said. UBS Group AG also cut their HSI target, citing weaker growth.

READ: China’s Economic Woes Are Multiplying and Xi Has No Easy Fix

After starting 2023 on a high note, traders have lost confidence as the second-leg of the reopening rally proved elusive. A key set of data showing manufacturing activity contracting and services losing steam also hurt sentiment. The CSI 300 is flat for the year, compared with double-digit gains in Japan, Taiwan, and South Korea. The HSI has lost more than 4%, among the worst performances in 92 primary indexes tracked by Bloomberg.

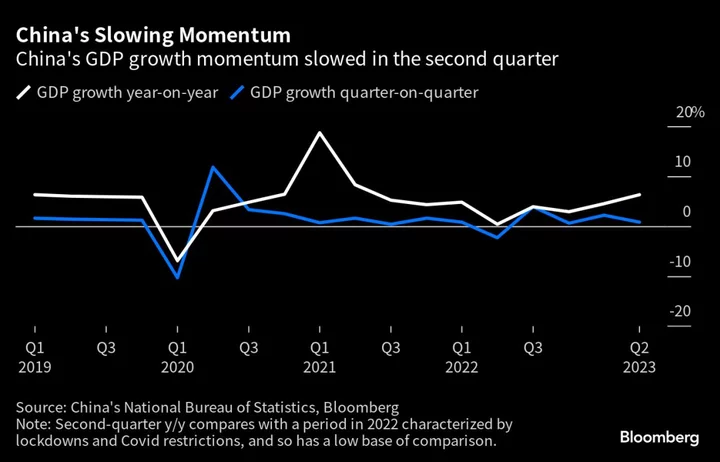

What’s troubling investors is that there seems to be no easy solution to China’s economic woes. Consumers are unwilling to spend, youth unemployment is at a record high, while manufacturers are struggling as demand softens at home and abroad. Towering local government debt and the yuan’s weakness suggest the room for aggressive easing via monetary and fiscal tools remains limited.

While respondents expect a range of about 7% to 11% gains for Hong Kong and mainland indexes through the end of the year, the projected levels remain below the highs reached at the end of January. The Shanghai Composite Index is an exception, with the forecast slightly above its May peak.

Overseas investors sold a net 2.7 billion yuan ($372 million) of mainland shares in the April-to-June period, marking the first quarterly outflow since September, according to data compiled by Bloomberg.

Bloomberg Survey

- Shows median estimate from survey of 18 respondents, some of whom didn’t give projections for certain gauges

To restore confidence, investors are calling for a ramp up of fiscal support in the way of consumption vouchers and tax breaks. Particularly pressing is the need to revive the property market as home price growth slows again. Market watchers are waiting for more meaningful measures to be announced, including the removal of purchase restrictions in high-tier cities.

Traders are hoping for catalysts from the July Politburo meeting, where top decision makers led by President Xi Jinping are expected to discuss new measures to boost the property and consumption sectors.

“I think it has become a consensus that something has to be done on the property policy front,” said Jizhou Dong, head of China property research at Nomura Holdings Inc. “If there is no meaningful rebound in property markets, investors will have a very bearish view toward the entire economy.”

Despite their muted expectations on returns, only one survey respondent said they will reduce China stock exposure in the coming months. The rest were split between those planning to add and those standing pat.

For some investors, the skepticism may be overdone. “China valuations could be too bearish at present and there’s room to be more constructive into the second half,” said David Chao, global market strategist for Asia Pacific at Invesco Asset Management. While none of the measures will be significant enough to move the markets in itself, they will be sizable once added up, he said.

BlackRock Investment Institute also held on to its overweight rating on China equities in its mid-year outlook, saying the bar for upside surprises is low given current valuations.

However, a slew of index target downgrades from major banks — with UBS joining the likes of Goldman Sachs Group Inc. and Morgan Stanley in reducing MSCI China forecasts — highlight growing bearishness. There’s also the potential that the Politburo meeting in July may disappoint — just like the State Council meeting in mid-June turned out to be an anticlimax with no concrete measures released.

--With assistance from Mengchen Lu, Charlotte Yang, Zhu Lin, John Cheng and Cynthia Li.