Once touted as a key driver of global oil profits, the plastics industry is staring down years of anemic margins as giant plants in China look set to send a deluge of production into the market.

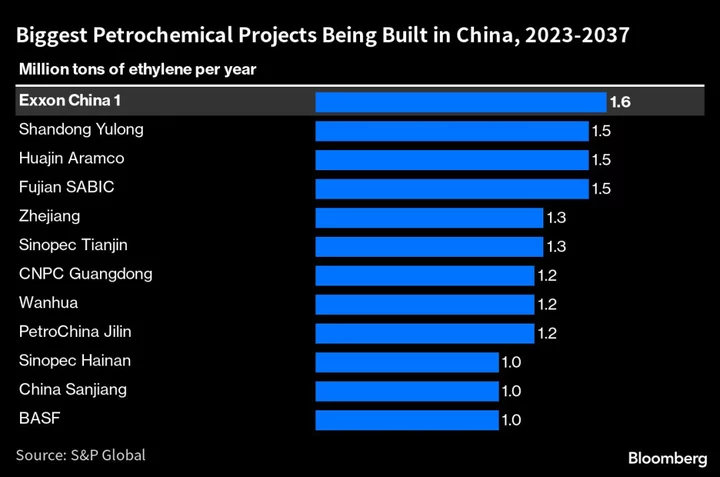

The construction of more than 20 petrochemical projects — to produce raw materials that go into making everything from plastic packaging to clothing and detergents — will be completed across China this year, said industry consultant ICIS.

While part of their output will go into factories across what is still the world’s largest consumer, a slower-than-expected rebound in China’s economy and excessive investment means oversupply is on the cards. As a result, returns for making petrochemicals such as ethylene and propylene are set to shrink, extending a malaise from this year when June margins stood at about 40% below 2019 levels.

China has been expanding enthusiastically in the industry as domestic demand growth for plastics began to outpace other oil-derived products such as transport and industrial fuels. While the initial idea was to move up the value chain and compensate for the drop in gasoline use as more people switch to electric cars, the completion of so many plants at once is setting the stage of a glut and squeezed profits, but also an overnight increase in market share and dominance.

Unable to take on more at home, China is exporting more cheap plastics into the rest of the region, eating into the market share of traditional manufacturing giants, such as South Korea and Japan. That’s bad news for large producers in the region like Formosa Plastics Corp., Lotte Chemical Corp. and GS Caltex Corp., now competing with China’s might.

“The market expected China’s recovery from the pandemic to be sharp and robust, but this has not happened,” said Salmon Lee, global head of polyesters at Wood Mackenzie. Now there’s supply that even growing markets such as Vietnam, Turkey, South Africa and India may not fully absorb.

In polyesters, for example, Chinese excess already means producers now see thin to no margins, Lee said.

Oversupply could come this year, says Larry Tan, vice president of chemical consulting in Asia at S&P Global Commodity Insights in Singapore. S&P sees global margins weak until demand and capacity rebalance in 2025.

Of the roughly 50 million tons of new ethylene capacity poised to come online from 2020-2024, nearly 60% will come from China, said Tan. He points out that the country’s increase in that period is 400% of current Japanese capacity.

And China continues to pour more investment into these plants. In May this year, Sinopec announced a 27.8 billion yuan ($3.85 billion) investment in a new plant in Luoyang city, poised to be completed in 2025, according to local media. Petrochemicals will also be at the core of Saudi Arabia’s latest investment in Rongsheng Petrochemical Co. Ltd.

“China has an advanced petrochemicals sector, the advantage of a huge and growing domestic market as well as potentially cost competitive output for exports,” said Michal Meidan, director of the China Energy Research Programme at the Oxford Institute for Energy Studies.

“As we have seen with BASF investments and the recent Saudi investments in China, it is clear that the country will be an important market even as it becomes a growing competitor.”

But for Western nations the question is the impact of China’s expansion. China’s petrochemical capacity will make up nearly a quarter of the world’s total by the end of this year, according to ICIS data. That’s a jump from five years ago, when it comprised just 14% of global manufacturing capacity. And it’s sizable at a time when China is flexing its muscles in other parts of the supply chain, while nations are fretting about supply disruptions and industrial security.

“China can leverage on its strength as the world’s leading refiner to also become the most important and competitive supplier of petrochemicals,” said John Driscoll, director of JTD Energy Services Pte in Singapore.

“The West will one day wake up to China as the single biggest supplier of all things plastics, as more mature economies in the US, Europe and places such as Australia drastically cut back on production without addressing their continued need for these materials.”

In light of those risks, nations such as India and Vietnam may choose to build their own production facilities on their own shores, says S&P’s Tan, arguing countries will weigh the return on investments against other objectives from national economic growth to jobs and reducing dependence on imports.

“This year and next year is the tipping point for the petrochemicals industry,” Lee added. “North Asian countries such as Japan, South Korea and Taiwan used to lead it, but now China will be a major force for years to come.”

--With assistance from Sarah Chen, Rachel Graham, Serene Cheong and Kevin Dharmawan.